Table of Contents

ToggleMoney Market Calculator (APY, Interest, and Growth Table)

Last updated: January, 2026

A money market calculator helps you estimate how much interest you will earn in a Money Market Account (MMA) or Money Market Fund (MMF). By entering your initial deposit, interest rate or APY, compounding frequency, and monthly contributions, you can forecast your total balance over a specific timeframe. This tool is essential for comparing different banking products to maximize your savings growth.

Money Market Calculator

Project your savings growth with compound interest, APY/APR conversion,

and regular contributions.

Assumes fixed rate over the term. For contributions, the frequency matches the compounding frequency.

Results

Final Balance—

Total Contributions—

Total Interest—

Effective APY:—

Assumed Periodic Rate (i):—

Compounds per Year (n):—

Total Periods (N):—

Chart unavailable. Calculation is correct; please ensure Chart.js is reachable.

Managing your cash effectively requires more than just picking a bank; it requires understanding how your money grows. Whether you are using a money market account calculator to plan for a rainy day or a money market fund calculator to manage investment liquidity, accuracy is key.

Ever wonder how much power is behind a vehicle? Use our horsepower calculator to find out instantly.

What This Money Market Calculator Does

This tool is designed to provide a clear picture of your potential savings growth. It moves beyond simple math to show the real-world impact of compounding and regular contributions.

What you can estimate:

- Ending Balance: Your total nest egg after a set period.

- Total Interest Earned: Exactly how much the bank or fund paid you for your deposit.

- The Power of APY: How different compounding frequencies (daily vs. monthly) change your bottom line.

Who it’s for:

- Savers comparing different banks or credit unions to find the best return.

- Planners who want to see how a $200 monthly deposit changes their 5-year outlook.

- Investors evaluating the “cash” portion of their portfolio.

Curious about the age gap between you and a friend, partner, or celebrity? Find out instantly with our age difference calculator.

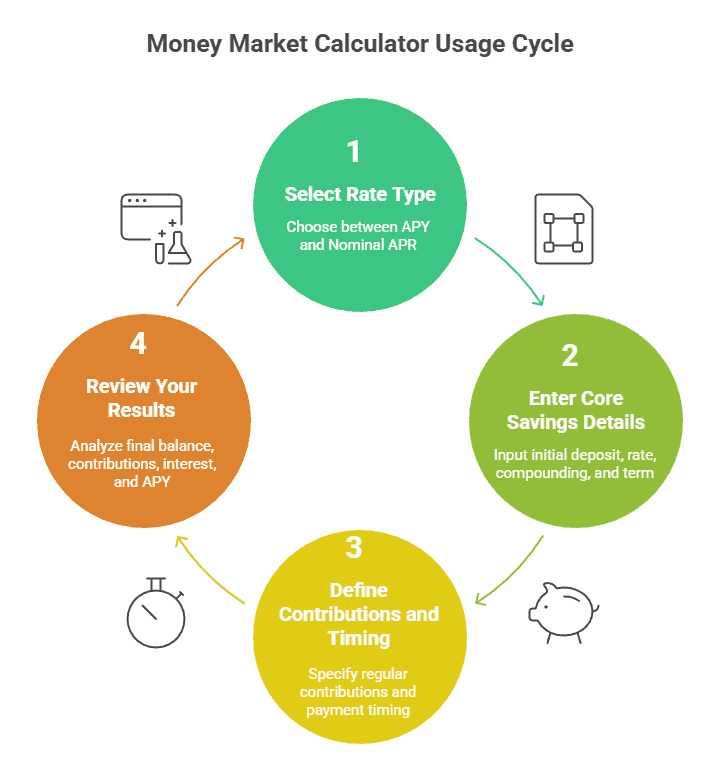

How to Use the Money Market Calculator

To get the most accurate result from a money market interest calculator, you need to gather specific data points from your bank’s website or your monthly statement.

This tool is designed to provide a fast, accurate forecast of your savings growth by accounting for initial deposits, recurring contributions, and the power of compounding. Follow these steps to generate your personalized savings projection:

Step 1: Select Your Rate Type

First, choose whether you are entering a % APY or a % Nominal APR.

- APY (Annual Percentage Yield): The effective annual rate that already includes the effect of compounding.

- Nominal APR (Annual Percentage Rate): The stated annual interest rate before compounding is applied.

Step 2: Enter Your Core Savings Details

Fill in the following fields based on your specific financial goals or account terms:

- Initial Deposit: Enter the starting balance you plan to put into the account (e.g., 50,000).

- Rate (%): Input the interest rate or APY provided by your bank or fund.

- Compounding Frequency: Select how often interest is calculated—such as Daily (365), Monthly (12), or Quarterly (4).

- Term: Define how long you plan to save by entering the total Years and Months.

Step 3: Define Contributions and Timing

If you plan to add more money over time, use these fields to increase the accuracy of your estimate:

- Regular Contribution (per period): Enter the amount you will deposit during each compounding period (e.g., adding 300 every month).

- Payment Timing: Choose End of Period (deposits made after interest is calculated) or Beginning (deposits made before interest is calculated).

Step 4: Review Your Results

Once you click Calculate, the tool provides a comprehensive breakdown:

- Final Balance: The total projected value of your account at the end of the term.

- Total Contributions: The sum of your initial deposit plus all recurring additions.

- Total Interest: The total amount of money earned strictly from interest growth.

- Effective APY: The true annual yield of your account.

- Growth Chart: A visual representation showing your balance climbing over the years.

Pro Tip: Save Your Data

After generating your results, you can use the Download PDF button to save a copy for your records or click Copy Summary to quickly paste the data into a spreadsheet or email.

Reminder: These results are educational estimates based on a fixed rate. Real-world rates for money market accounts and funds are subject to change over time.

Would you like me to generate a step-by-step guide on how to specifically find these rates and compounding details on your bank statement?

Money Market Account vs. Money Market Fund

While they sound similar, these two products are governed by different regulations and carry different risks.

Feature | Money Market Account (MMA) | Money Market Fund (MMF) |

Type | Deposit Account at a Bank/Credit Union | Investment Fund (Mutual Fund) |

Insurance | FDIC (Banks) or NCUA (Credit Unions) | Generally Not Insured (SIPC may apply to broker failure) |

Returns | Interest Rate / APY | Dividend Yield |

Risk | Virtually None (up to insurance limits) | Low, but possible to lose value (“break the buck”) |

Regulation | FDIC / NCUA / CFPB | SEC / FINRA |

Our calculator defaults to money market account calculator logic, but it can be used for funds by entering the fund’s “7-day SEC yield” as the interest rate.

Stop signing up! Start writing instantly with our 100% private, No-Login Online Notepad that keeps notes securely on your device.

Money Market Interest Calculator (How the Math Works)

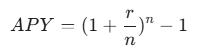

Understanding the difference between the nominal interest rate and the Annual Percentage Yield (APY) is vital for any annual percentage yield calculator user.

Interest Rate vs. APY

The interest rate is the base percentage the bank pays. 56The APY is the “effective” rate—it tells you what you actually earn after interest is added back into your balance and begins earning its own interest.

The APY Formula

- r = nominal annual interest rate (as a decimal)

- n = number of compounding periods per year

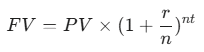

The Compound Interest Formula

For a lump sum with no additional deposits:

- FV = Future Value

- PV = Present Value (Starting Balance)

- t = Time in years

When you add monthly contributions, the math involves the future value of an annuity formula, assuming deposits are made at the end of each period.

Stop wasting money on materials—use our Stone Calculator to find the exact volume and weight of gravel or stone your project requires and order the precise amount.

Worked Examples

Example 1: Standard Money Market Account

- Starting Balance: 10,000

- APY: 4.50%

- Compounding: Monthly

- Timeframe: 1 Year

- Result: 10,459.40 (Interest Earned: 459.40)

Example 2: Account with Monthly Contributions

- Starting Balance: 10,000

- Monthly Deposit: 500

- APY: 4.50%

- Timeframe: 1 Year

- Result: 16,583.56 (Interest Earned: 583.56)

- Note: Adding just 500 a month significantly increased the total interest earned because there was more principal to compound.

Paying Zakat is a vital pillar of faith, but calculating it correctly can feel overwhelming. That’s where the Sahaj Tools Zakat Calculator comes in — designed to make your spiritual obligation effortless, accurate, and stress-free.

Compound Interest Tables (See Growth Over Time)

A compound interest table provides a visual roadmap of your savings.

Year | Starting Balance | Annual Contribution | Interest Earned | Ending Balance |

1 | 10,000 | 2,400 | 478 | 12,878 |

2 | 12,878 | 2,400 | 612 | 15,890 |

3 | 15,890 | 2,400 | 753 | 19,043 |

4 | 19,043 | 2,400 | 900 | 22,343 |

5 | 22,343 | 2,400 | 1,054 | 25,797 |

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a $200 monthly deposit.

Assumes 4.00% APY compounded monthly with a 200 monthly deposit.

How to Calculate Interest on a Savings Account

While our money market rate calculator handles the complex math, you can use a “back-of-the-napkin” method for simple interest:

Interest = Principal × Rate × Time

However, most modern accounts use compound interest. A savings interest calculator or a simple savings calculator is often enough for basic accounts, but money market accounts often have higher balances and tiered rates that require the precision of a dedicated money market account calculator.

Money Market vs. High-Yield Savings Calculator

When choosing between a high-yield savings calculator and a money market calculator, consider your access needs:

- Money Market Accounts: Often include check-writing abilities or debit cards. They may require higher minimum balances to avoid fees.

- High-Yield Savings Accounts (HYSA): Typically offer similar rates but may have fewer “transactional” features.

- The Bottom Line: If the rates are identical, use a high-interest savings account calculator to see if the flexibility of an MMA is worth any potential fees.

Common Questions About Money Market Accounts (FAQs)

Technically, the math is the same. However, a money market account calculator is better for accounts with tiered interest rates and higher minimum balance requirements common to MMAs.

For simple interest, multiply your principal by the rate and time. For compounding, use the formula FV = PV(1 + r/n)^nt.

Rates vary based on the Federal Reserve's actions. Use a money market rate calculator to compare your current bank against national averages found on the FDIC website.

No. Money market funds are investment products regulated by the SEC. Only money market accounts at banks are insured by the FDIC.

Most compound daily and credit interest monthly. Check your deposit agreement for your specific "n" value for the annual percentage yield calculator.

As long as the bank is FDIC-insured and you are under the 250,000 limit, your principal is safe. However, fees or inflation can reduce your "real" purchasing power.

A cash on cash return calculator is usually for real estate, measuring annual cash flow against the initial cash invested. It is less common for standard money market accounts.

Because the APY reflects compounding. When your interest earns interest, your "yield" increases

Many do if you fall below a certain minimum balance. Always subtract potential fees from your calculator results for an accurate forecast.

Compare the APYs of multiple institutions. Ensure you are comparing "apples to apples" by checking the compounding frequency on each.

Financial Accuracy Disclaimer

This content and the associated calculator tool are for educational and illustrative purposes only. They do not constitute financial, tax, or legal advice. Interest rates, Annual Percentage Yields (APY), and terms are subject to change and vary by institution. Results are estimates and may not account for specific bank fees, taxes, or tiered-rate structures unless manually adjusted. Always verify current rates and terms with your financial institution or fund provider before making a decision.

Reference List

- FDIC (Federal Deposit Insurance Corporation): Understanding Deposit Insurance.

- NCUA (National Credit Union Administration): Share Insurance Basics.

- SEC (Securities and Exchange Commission): Money Market Funds Investor Bulletin.

- FINRA: Evaluating Investment Risk.

- CFPB (Consumer Financial Protection Bureau): Guide to Savings and Money Market Accounts.

- Principles of Finance (Standard Math References): Compound interest and annuity formulas.